First-time home buyers

Buying your first home can feel confusing fast. DoorLine gives you plain-English education and helps you get matched, at no cost, with a licensed local real-estate agent so you can compare your options and choose who to work with.

What first-time buyers should know before they start

A first home is exciting, but it is also a big contract with real money at stake. You do not need to know everything on day one. You do need to understand the basic steps, the common costs, and where people get pressured into signing too fast.

In general, most first-time buyers need to plan for:

- Down payment: often about 3% to 20% of the price, depending on the loan and your situation

- Buyer closing costs: often about 2% to 5% of the price

- Monthly payment: usually principal, interest, property taxes, homeowners insurance, and sometimes HOA dues or mortgage insurance

- Cash after closing: for moving, repairs, utilities, and normal surprises

Real numbers depend on the home, the price, the location, the loan, and the agreements you sign.

DoorLine is not a brokerage, agent, lender, or law firm. We do not give real-estate, mortgage, legal, tax, or financial advice. We provide general education and a free matching service that helps you compare licensed local agents. If you are just starting, see buying a home or first-time buyer basics.

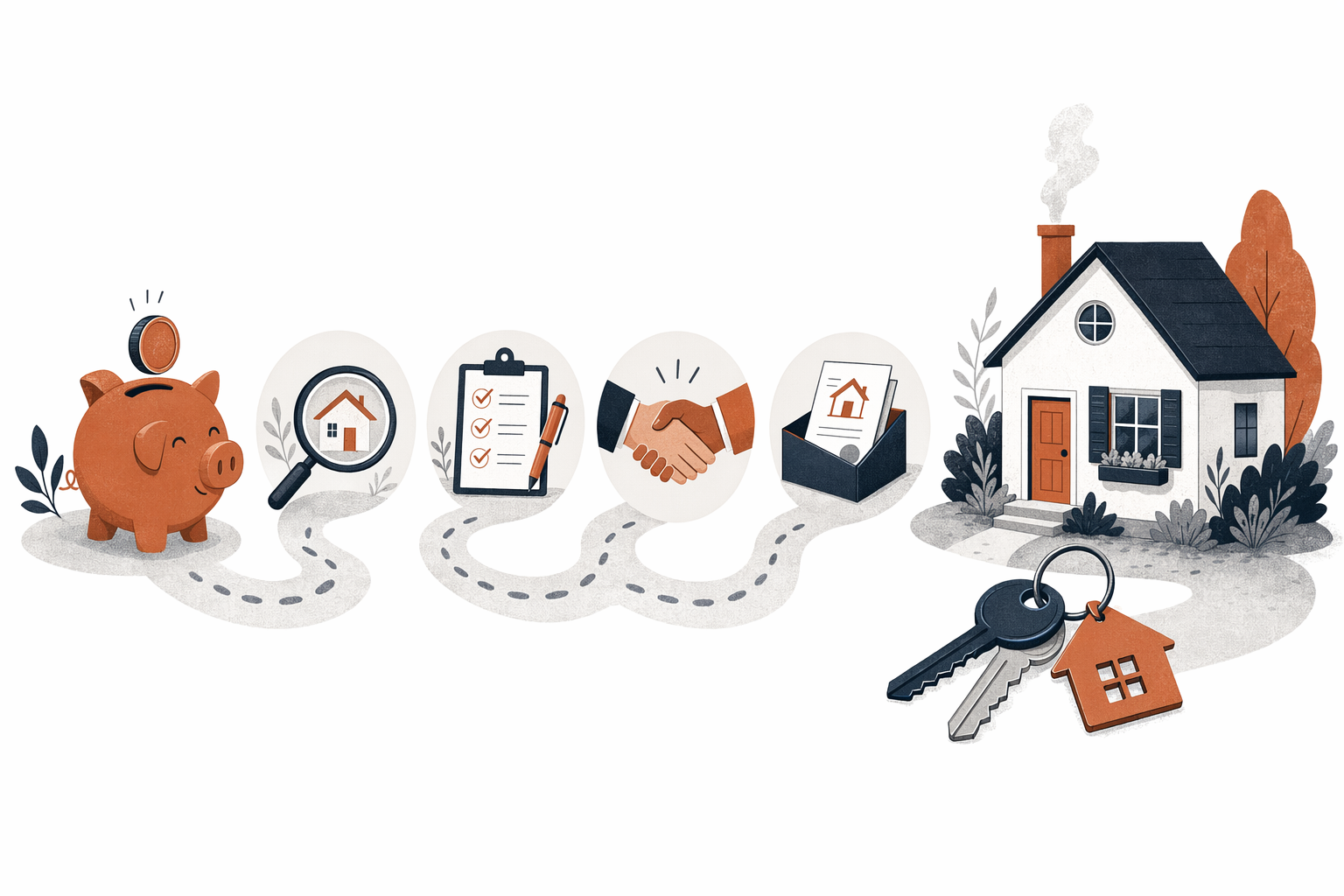

How the buying process usually works

Here is the simple version of how many first purchases go:

- Set a real budget. Think about monthly payment, cash to close, and cash left after closing.

- Talk to a licensed lender if you plan to use a mortgage. Ask what loan programs may apply and what paperwork they need.

- Compare licensed agents. You are allowed to ask questions, compare communication styles, and choose the person you trust.

- Tour homes. Focus on price, condition, commute, public data, and features that fit your life.

- Make an offer. The written offer can include price, timing, inspections, and other terms.

- Do inspections and final loan steps. Read deadlines carefully. Missed deadlines can cost you money.

- Review closing documents. Confirm all fees in writing before signing.

- Close and get the keys. If money is being wired, confirm wiring instructions by phone using a trusted number before sending anything.

A good agent should explain each step in plain language. A good lender should do the same for the loan side. Always work with licensed professionals, verify any license yourself, and read every agreement before you sign.

If you want help finding agents to compare, you can get matched for free.

What it usually costs to buy your first home

A lot of first-time buyers focus only on the down payment. That is a mistake. The full picture matters.

Common upfront costs

- Earnest money deposit: a good-faith deposit that may be applied at closing, depending on the contract

- Down payment: often 3% to 20%

- Closing costs: often 2% to 5%

- Inspection and related reports: common in many transactions

- Appraisal or lender fees: if required by the loan

- Moving and setup costs: truck, locks, utility transfers, small repairs, furniture

Buyer-agent compensation

Buyer-agent compensation is increasingly negotiable and the structure can vary by market and agreement. In many transactions, a seller may offer compensation to the buyer's agent, but not always. A common range people hear is around 2.5% to 3% per side, but that is not a rule, not guaranteed, and not the same in every deal. Read your written agreement and confirm how your agent is paid before you sign.

Monthly costs after you close

- Mortgage principal and interest

- Property taxes

- Homeowners insurance

- Mortgage insurance if applicable

- HOA dues if applicable

- Maintenance and repairs

Use estimates, not hope. Ask for a written cost breakdown and compare it line by line. For more detail, read closing costs explained and home-buying costs.

A realistic timeline for first-time buyers

Some buyers close in about 30 to 45 days after a contract is accepted. Others take longer because they are still saving, improving credit, comparing lenders, or waiting for the right home.

A realistic first-time timeline often looks like this:

- 2 to 8 weeks to prepare: budget, documents, lender conversations, agent interviews

- 2 to 12+ weeks to shop: depends on inventory, price range, and how selective you need to be

- 30 to 45 days under contract: inspections, appraisal, underwriting, final review

What slows things down?

- Changing jobs during the loan process

- Large new debts or big purchases

- Missing lender documents

- Homes with condition problems

- Appraisal gaps

- Title issues or delayed paperwork

What speeds things up?

- Having documents ready

- Answering requests quickly

- Staying inside your budget

- Working with a responsive licensed agent and lender

Do not let anyone rush you by saying you must sign now or lose everything. Sometimes homes move fast. That is real. But pressure is not the same as good advice. Slow down enough to understand the numbers and the contract.

What to ask before you choose an agent

You are not hiring a best friend. You are choosing someone to help you through a major transaction. Interview more than one person if you can.

Ask questions like:

- How do you help first-time buyers understand the process?

- How will we communicate, and how often?

- Have you worked with buyers in my price range and timeline?

- What fees or agreements do you want me to sign, and when?

- How is your compensation handled in my market and under this agreement?

- What happens if I decide not to buy right away?

- How do you help buyers compare homes without pressure?

- How do you handle inspections, repair requests, and deadlines?

You should also ask for the agent's license information and verify it yourself with the state. Read the agreement carefully. Confirm cancellation terms, timing, and any fees in writing.

If you want a framework, read how to choose a real-estate agent. DoorLine can help you compare licensed local agents, but you choose who to work with.

Your rights as a buyer

You have rights. Knowing them can protect your money and your peace of mind.

Fair Housing matters

DoorLine follows the Fair Housing Act. All buyers and sellers are welcome. No one should steer you toward or away from a neighborhood, home, or agent because of race, color, religion, sex, disability, familial status, national origin, or other protected characteristics. When comparing areas, focus on lawful, objective factors like commute, price, property taxes, public school data, transportation, and nearby services, not assumptions about who lives there. Learn more about your fair housing rights.

You have the right to compare

- Compare agents

- Compare lenders

- Compare homes

- Read every agreement before signing

- Ask questions until you understand the answer

You have the right to written terms

Important terms and fees should be in writing. If a number changes, ask why. If something sounds verbal and vague, ask for written confirmation.

You have the right to be careful with money movement

Wire fraud is real in real estate. If you need to send money, confirm instructions by phone using a trusted number you found independently, not a number from a suspicious email or text.

How DoorLine helps first-time buyers

DoorLine is for people who want honest information and a better way to start. We are especially helpful for buyers who may feel overlooked or confused, including new immigrants, ITIN buyers, first-time buyers, and non-native-English speakers.

What we do:

- Explain the process in plain, general terms

- Help you understand what questions to ask

- Match you, for free, with licensed local real-estate agents you can compare

- Let you decide who to talk to and whether to move forward

What we do not do:

- We do not act as your agent or brokerage

- We do not provide loans or legal services

- We do not tell you which home to buy

- We do not guarantee prices, approval, savings, or outcomes

The matching service is free to consumers. Participating agents pay DoorLine a flat marketing fee. That means you can compare options without paying DoorLine to be introduced.

If you are ready, get matched. If you still want to learn first, first-time buyer help is a good next step.

Start with your budget, learn the real costs, compare licensed agents, and do not sign anything you do not understand. DoorLine is free to you and can help you find local agents to compare, but you stay in control and choose who to work with.